Fueled by the advance of technology, flexibility of remote work, continued expansion of global business, and desirable cost of living tradeoffs for retirees, the ranks

COVID-19: A Comprehensive Guide to Navigating the New Financial Planning Landscape

Published Date : April 9, 2020

April 9, 2020

The recent and significant volatility in the capital markets has caused a lot of trouble and worry, on many fronts; not to mention our collective personal health and safety concerns. Although equity markets are down significantly from their highs just a month ago, there are various personal financial planning strategies that could warrant immediate attention, and many others that present very compelling long-term opportunities with the right circumstances and resources.

Please contact your Wealth Manager at Sand Hill Global Advisors if you would like more information on any of the topics outlined here or to analyze and explore any of these ideas further. As is always the case, these broad observations are general in nature, and each individual’s case is unique and different; so, please be sure to discuss any and all relevant concepts with your accountant and/or estate attorney, as necessary, to avoid any unintended personal consequences.

Below are some potentially constructive action items to currently consider. Please use the links below to jump straight to any topics of particular interest:

TAX CONSIDERATIONS

Tax Filing and Payment Deadline Changes

RETIREMENT ACCOUNTS

2020 Required Minimum Distributions (RMDs) Are Exempted

There’s Still Time to Make 2019 IRA Contributions

Roth IRA Conversions in a Volatile Market

INVESTMENT CONSIDERATIONS

A Good Time to Invest?

Continue Your Savings Plans

The Value in Tax-Loss Harvesting

LIQUIDITY NEEDS

The World Changed Quickly. Do You Have Enough Cash in Emergency Reserve?

Consider Other Sources of Liquidity Besides Savings

Using Retirement Accounts for Emergency Cash Needs

ESTATE PLANNING OPPORTUNITIES AND GIFTS TO FAMILY

Loans to Family, Using Attractively Low Applicable Federal Rates (AFR)

Possible Gifting Advantages with Suppressed Stock Valuations

Consider Funding Grantor Retained Annuity Trusts (GRAT)

FINANCIAL WELLNESS

There’s No Better Time Than the Present to Review Your Financial Plan

Risk Management – Now’s a Good Time to Review Your Insurance Policies

Be on High Alert for Scammers

The Stimulus Package and Payroll Taxes

SBA Loans for Small Business Owners

Direct Payments for Eligible Individuals and Children

Mortgage Refinancing Amid an Historic Interest Rate Decline

Be Mindful of Your Budget

WHAT CAN YOU DO TO HELP NOW?

Financial Education as Our Children Look to Us for Guidance

Charitable Giving

TAX CONSIDERATIONS

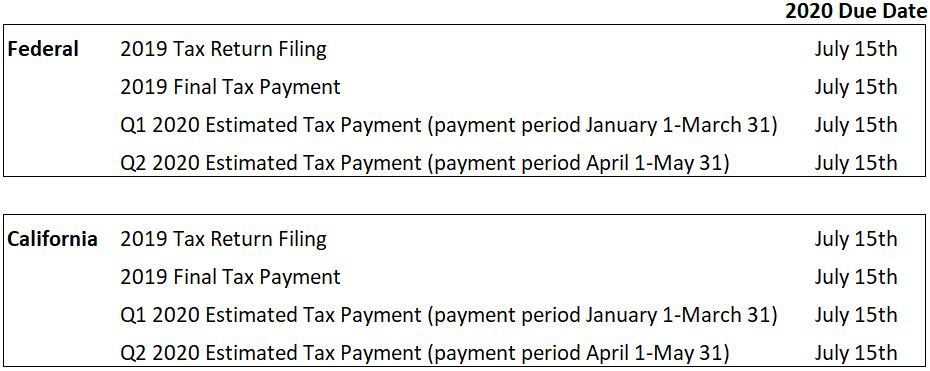

Tax Filing and Payment Deadline Changes

Action: Contact your accountant to confirm how these changes apply to you.

Good news: You have a few more months to finalize your personal income taxes! For Federal and California income taxes, below are the tax filing and payment deadlines that have been recently adjusted to July 15th1:

The traditional April 15th tax day has been moved to July 15th, and there will be no adverse consequences to taxpayers who wait up until July 15th to file and pay their tax liability. Of course, if possible, it is always recommended to file earlier when a refund is due to the taxpayer, as the IRS is continuing to pay those refunds out. The 1st and 2nd quarter 2020 estimated tax payments, normally due on April 15th and June 15th respectively, have also been pushed to July 15th. All of the changes covered here are specific to Federal income taxes, but many states, including California, have followed suit.

RETIREMENT ACCOUNTS

2020 Required Minimum Distributions (RMDs) are Exempted

Action: No RMDs for 2020

For those IRA owners who do not rely on their Traditional or Rollover IRA to provide income to help meet general living expenses, the recent Coronavirus Aid, Relief and Economic Security (CARES) Act allows them to forgo their RMD this year.2 Our understanding is this change applies to Inherited IRA RMDs as well. This could be helpful for two reasons: the RMD is always based on the December 31st account value of the preceding year (so 12/31/2019 values are used to calculate RMDs for 2020); and that value has likely since fallen, perhaps quite a bit. Taking that higher RMD withdrawal amount from a now lower account value puts an extra burden on the resulting account size. Also, RMDs create taxable income, and all things considered, it might not be helpful to add to taxable income this year.

There’s Still Time to Make 2019 IRA Contributions

Action: Consider funding your IRA by the new tax-filing deadline of July 15th.

By extending the tax filing deadline, taxpayers are now allowed extra time to save money to contribute to their IRA and Health Savings Account (HSA). It is also beneficial to those who strive to maximize their contributions but need extra time to determine if these funds will be necessary to cover daily expenses through times of economic uncertainty. Remember that you must indicate that your contribution is for 2019 so it is not erroneously applied against the 2020 tax year.

As a reminder, the current maximum annual contribution amount for both Roth and Traditional IRAs is $6,000 for an individual, plus an additional $1,000 if you are 50 and over. The maximum HSA contribution is $3,500 for self-coverage, plus an additional $1,000 catch-up contribution for those individuals who are 55 and older. If you have a spouse or dependents on your health plan, the maximum amount increases to $7,000.1

Roth IRA Conversions in a Volatile Market

Action: Possible opportunity to convert your Traditional IRA to a Roth IRA

This difficult period in the financial markets could nonetheless be a great opportunity to convert some—or possibly all—of your Traditional or Rollover IRA assets into a Roth IRA. Because asset values are down, the conversion amount would also be suppressed, resulting in less tax on the conversion. The primary consideration is that you pay ordinary income taxes now on any conversion amount; so, this needs to be carefully examined and reviewed with your tax advisor to gauge your overall income and tax situation. In return, unlike the tax deferral of a regular IRA, all future growth in the Roth IRA is never taxed. Plus, there are no RMDs for a Roth IRA owner; hence, the Roth IRA owner never has to take money out.

Furthermore, a logical assumption for longer term planning is that ordinary income tax rates are apt to increase, especially considering the recently passed $2.2 trillion Congressional bailout package—and possibly more stimulus to come. So, by completing a Roth IRA conversion this year, you’ll be paying tax at what could be a lower tax rate now.

INVESTMENT CONSIDERATIONS

A Good Time to Invest?

Action: Consider what to do with any significant cash on the sidelines.

Investors who came into the recent market drop with excess cash on the sidelines are obviously feeling good about that positioning. However, the severity of the decline now begs the question of whether some of that money should be invested (per existing portfolio strategy). We are not suggesting definitively that the market bottom has been hit; but for the long-term investor, the entry point for putting new money to work is relatively more attractive now than just a month ago. Staggering in any such commitments is a sensible way to approach this.

Of course, cash is king in any type of crisis, so the ongoing maintenance of any earmarked or required cash reserve should be part of that decision-making process.

Continue Your Savings Plans

Action: Continue 401(k) contributions and 529 plan funding.

During difficult financial markets such as this one, it is important to not lose sight of one’s true time horizon—typically measured in years, if not decades—and hence not abandon or alter well-laid (and possibly automatic) plans to fund accounts to meet long-term objectives. If possible, 401(k) retirement accounts should continue to be funded, especially if one’s employer matches.

If additional resources are available, it could also be a good time to fund 529 (education) plans for young relatives. Since those accounts will presumably grow over many years, this could be a good entry point for making such gifts and corresponding investments.

The Value in Tax-Loss Harvesting

Action: Selling a security at a loss, and offsetting other possible realized gains on the year (or carrying forward the losses to future years)

As painful as it is, volatile markets also offer potential opportunities to create value. Tax-loss harvesting involves selling a security to realize that loss, and then typically immediately buying another similar—but not identical—security to maintain proper portfolio exposure. These losses can be used to offset capital gains in the current year or be rolled over into future years and similarly applied to gains. When tax-loss harvesting, it is very important to avoid violating Wash Sale rules, as the IRS does not permit investors to simply rotate through the same position for the purpose of continuously generating losses. Harvesting losses is a strategy that we at Sand Hill actively address on your behalf where appropriate.

LIQUIDITY NEEDS

The World Changed Quickly. Do You Have Enough Cash in Emergency Reserve?

Action: Review your monthly cash need and make sure you have an appropriate reserve.

A pandemic is unfortunately a great time to make sure you have an adequate emergency savings reserve. Typically, this money is enough to cover basic expenses for 3-6 months (3 if two-earner household, 6 if one-earner or if job security is in question). The objective is safety, so we recommend the money be kept in a very short-term, conservative and liquid investment, such as a money market vehicle. We definitely prioritize safety over trying to maximize yield with these funds. Please note, basic expenses will likely be lower than a typical budget, as the shelter-in-place mandates mean we are not going out to dinner or spending money on entertainment and travel.

Consider Other Sources of Liquidity Besides Savings

Action Item: Think about tapping into your HELOC or life insurance policies for liquidity.

You’ve heard the advice to stay the course with your portfolio strategy and minimize withdrawals where possible, but when you need liquidity for a home repair or another of life’s emergencies, where else could you turn? A new or existing Home Equity Line of Credit (HELOC) could be a good source of cash in the current low interest rate environment. Over the long-term, your investment portfolio should perform better and earn more for you than what you’d pay in interest on the HELOC.

Another often overlooked source of liquidity is the cash balance in whole life insurance policies. Many policies allow for the tax-free withdrawal of your cost basis—what you’ve paid over the years in the form of premiums—while keeping the life insurance component of the policy intact. Your life insurance policies should be analyzed to determine if this strategy is appropriate for your situation and it is worth digging out your most recent statement to review.

Using Retirement Accounts for Emergency Cash Needs

Action: If you’ve been directly affected by COVID-19, your retirement accounts could provide emergency liquidity.

For some, instead of making contributions right now to retirement plans, there could be withdrawal needs. The recent CARES Act includes provisions for either a straight withdrawal or a loan from a 401(k). IRAs don’t permit loans. The law temporarily loosens the rules on hardship distributions from retirement accounts giving those directly affected by COVID-19 access to their retirement savings. The new rules apply to a whole range of people, including those who have lost a job because of the pandemic, those suffering from COVID-19 or who have a spouse with the virus. If you meet the qualified individual criteria, the typical early withdrawal penalty of 10%, applied when you take a distribution before age 59½, will be waived.

The rules around these provisions differ:

Loan From a 401(k):

- The Act now allows for an increase in the hardship loan maximum that 401(k) plan participants can withdraw to up to the lesser of either $100,000 or 100% of the vested account value.

- The participant won’t owe income tax on the amount borrowed from the 401(k) if it’s paid back within five years, according to the American Retirement Association.

Straight Withdrawal:

- The Act allows for straight withdrawals taken in 2020 of up to $100,000 from employer-sponsored retirement plans and/or IRAs.

- In addition, if the account holder replaces the money within three years, they also will be able to recover the federal and state income taxes that apply to the withdrawal, according to the American Retirement Association.

Finally, try other forms of assistance first; it is not ideal to deplete retirement savings, especially when retirement accounts are down in value.

ESTATE PLANNING OPPORTUNITIES AND GIFTS TO FAMILY

Does Your Family Need Financial Assistance? Is This an Opportunity to Engage or Continue Estate Planning Strategies?

While interest rates are at historically low levels and asset values are depressed, now is a good time to review your current gifting strategies. Do they still make sense in the current environment? If you have been thinking about making outright gifts to your children or grandchildren to reduce your taxable estate, the current market environment could work to your advantage over the long-term. Here are some impactful strategies to consider during this most unusual time:

Action: Loans to family, using attractively low Applicable Federal Rates (AFR)

The IRS allows loans to family members—to avoid the transfer of funds being treated as a gift—as long as the Applicable Federal Rate (AFR) of interest is charged. The AFR will depend on the time period for the loan: short (3 years or less); medium (3 to 9 years); or long (9 years or more). The current low overall interest rate environment and yield curve has favorably impacted the AFR, especially on the long end. If financial assistance is needed in the moment, this could be an effective way to provide help amongst family members.

Action: Possible gifting advantages with suppressed stock valuations

Gifting low-basis stocks with currently suppressed trading prices and yet still high future appreciation potential could be advantageous. The maximum annual exclusion gift per person in 2020 remains $15,000 per person per year (or $30,000 gift per couple). Often this type of gifting is done with cash, but stock could be useful. If the stock recipient holds the stock long enough to experience a market recovery, which often follows major market declines, a larger gift transfer would have been accomplished. Note: The existing cost basis transfers to the recipient, so this needs to be fully examined and understood prior to taking action.

Action: Consider funding Grantor Retained Annuity Trusts (GRAT).

A GRAT is an effective way to make potentially significant gifts to family while reducing your taxable estate. A GRAT allows for a gift of assets to an irrevocable trust whereby if the grantor outlives the established term (2‐3 years up to 15 years) and the return on the gifted assets is greater than the IRS 7520 “hurdle rate”, what remains in the trust at the end of the specified term can be transferred to beneficiaries free of tax. With historically low interest rates and the renewed opportunity for market appreciation, GRATs have again become a potentially compelling wealth transfer strategy.

FINANCIAL WELLNESS

There’s No Better Time Than the Present to Review Your Financial Plan

Action: Take inventory of your priorities.

As we are sequestered at home, many of us suddenly have more time on our hands. This is a great opportunity to revisit details related to your financial planning that may have fallen through the cracks. Is your estate plan up to date? Do you have extra memberships you’re not using that would make sense to cancel? Do you have any credit cards you no longer utilize? Do your cell phone and cable plans need modifying? Taking video and/or photos of your household inventory is a worthwhile activity to ensure you have documented your belongings in the event of a fire or earthquake. An inventory list in a spreadsheet is also a good idea.

Risk Management – Now’s a Good Time to Review Your Insurance Policies

Action: Review insurance policies for adequate coverage.

Adults reliant on earned income should review their employee benefits to ensure adequate health and disability insurance coverage would be available in the event of a prolonged illness. Life insurance policies should also be reviewed to ensure that death benefits adequately cover expected expenses should income stop due to the loss of a family provider. For those losing health insurance due to unemployment, exploring the availability and cost of 18 months of COBRA insurance coverage (or one’s state market health plan options) should be done within 60 days of job loss.

Be on High Alert for Scammers

Action: Always be cautious when receiving phone calls, emails or texts from unknown sources – be aware of latest scams related to the Coronavirus.

Coronavirus or not, scammers never take a break and public fears of the pandemic has offered them a new opportunity to scare people into turning over sensitive personal information and money. Some examples include calls and texts offering potential treatments or test kits or tempting the recipient with offers related to the stimulus act, such as, “Click here to claim your benefits.”

Scams are not new of course, but COVID-19-related messages are one of the newest types of text scam. Below are some tips from the Federal Communications Commission (FCC) on what to do—and what not to do—when you receive a spam text.

- Do not respond to calls or texts from unknown numbers, or any others that appear suspicious.

- Never share your personal or financial information via email, text messages, or over the phone.

- Be cautious if you’re being pressured to share any information or make a payment immediately.

- Scammers often spoof phone numbers to trick you into answering or responding. Remember that government agencies will never call you to ask for personal information or money.

- Do not click any links in a text message. If a friend sends you a text with a suspicious link that seems out of character, call them to make sure they weren’t hacked.

- Always check on a charity (for example, by calling or looking at its actual website) before donating.

The Stimulus Package and Payroll Taxes

Action: You still need to report and pay payroll-related taxes.

Although the CARES Act offers several benefits for small business owners, you cannot defer reporting or paying payroll-related taxes. However, the Act does allow for deferral of the employer portion of social security taxes. Specifically, employers and self-employed individuals can defer over two years the payment of the employer’s portion of the 6.2% Social Security payroll tax imposed on employee wages paid between March 27, 2020, and December 31, 2020. Self-employed individuals also qualify for the deferral and should consider reducing their quarterly estimated tax payments. Taxpayers must pay one-half of the deferred amount by December 31, 2021, and the other half by December 31, 2022.

SBA Loans for Small Business Owners

Action: Small business owners should visit the SBA website to learn what financial assistance is available.

Most small business owners are familiar with the Small Business Administration (SBA). There are new provisions for small businesses under the CARES Act. Accessing information and funds may require some patience as the SBA continues to work out some of the details. Specifically, the CARES Act establishes the following new options:

- Paycheck Protection Program – This loan program provides loan forgiveness for retaining employees by temporarily expanding the traditional SBA loan program. The program is designed to provide a direct incentive for small businesses to keep their workers on the payroll. The SBA will forgive the loan if all employees are kept on the payroll for eight weeks and the money is used for payroll, rent, mortgage interest, or utilities.

- Economic Injury Disaster Loan Emergency Advance (EIDL Loan Advance) – This loan advance will provide up to $10,000 of economic relief to businesses that are currently experiencing temporary difficulties.

- SBA Express Bridge Loans – This enables small businesses who currently have a business relationship with a SBA Express Lender to access up to $25,000 quickly in the form of a SBA Express Disaster Bridge Loan. This is for a small business that has an urgent need for cash while waiting for a decision and disbursement on an Economic Injury Disaster Loan.

- SBA Debt Relief – The SBA is providing a financial reprieve to small businesses during the COVID-19 pandemic. Specifically, the SBA will pay the principal, interest and fees for existing and new microloans for six months.

Direct Payments for Eligible Individuals and Children

Action: Possible receipt of direct stimulus payment from the CARES Act

Eligible adult taxpayers earning up to $75,000 in income shall receive $1,200 ($2,400 per couple earning up to $150,000) via direct deposit or mailed checks. The payment amount will be based on the adjusted gross income (AGI) reported on their 2019 tax return (or 2018 tax return if 2019 is not complete). An additional $500 direct payment will be made for each child (under age 17) in such eligible family. Complete phaseout for receiving the direct payment will be at $99,000 (AGI) for a single adult and $198,000 for couples. For those who qualify in 2020 but not in 2019, no direct payment will be made; but a credit can be applied on the 2020 tax return.

Mortgage Refinancing Amid a Historic Interest Rate Decline

Action: Mortgage rates are tied to Treasury rates, which have recently hit historic lows. This is now possibly a good time to refinance existing mortgage terms.

Recent market volatility hasn’t been isolated to just the equity market; interest rates—across the yield curve—have also fallen to historic lows as a result of investors flocking to the relative safety of fixed income. Since mortgage rates are tied to Treasury rates, a decline in mortgage rates has similarly ensued. There may be an opportunity for certain borrowers to meaningfully reduce monthly mortgage expenses by refinancing, if the new going rate on mortgages is enough to move the needle.

Due to this historic movement, mortgage brokers are presently under a great deal of strain to keep up with the wave of this refinance demand and some loan programs are shut down all together. Therefore, there will be delays in this process.

Be Mindful of Your Budget

Action: Review your current cash flow to make sure you are still on track to attain your financial goals.

If your income has been reduced or you suspect that you may face potential loss of employment, start by creating a list of all expenses. You need a clear understanding of all essential costs. You should also create a list of all non-essential expenditures. This list will include items such as gifts to charity and family members, subscriptions, gym and club memberships. From here, you can then prioritize the list as you determine which expenses can be targeted for reduction or elimination.

WHAT CAN YOU DO TO HELP NOW?

Financial Education as Our Children Look to Us for Guidance

Action: The current situation could provide unique “teaching moments” for youngsters.

We are passionate about financial literacy for children and young adults and the past few weeks have presented a truly unique opportunity to connect with our younger generation. This experience is fast becoming an integral and lasting part of all our lives and will be talked about for generations to come. Engaging with them during this time of turmoil and uncertainty with regard to various money topics—from budgeting, to discretionary spending, to charitable contributions, etc.—will further help to build a constructive foundation from which they can shape their personal financial future. These teaching moments will help form their understanding of the world as their own financial lives evolve over time.

Charitable Giving

Action: If you can afford to, continue gifting to charity, as they need those funds now more than ever!

The CARES Act includes a few updates to charitable giving rules that are in place for 2020 gifts only. Previously, the deductibility of direct cash gifts to public charities was limited to 60% of Adjusted Gross Income (AGI). The CARES Act relaxes this limit for 2020 gifts by allowing taxpayers to deduct up to 100% of AGI if cash is gifted directly to public charities. It’s important to note that this higher deductibility limit does not apply for gifts made to Donor Advised Funds. Also, the CARES Act did not change the charitable deduction limit for non-cash gifts.

Prior to 2020 and starting again in 2021, taxpayers are required to itemize deductions and list their charitable gifts on Schedule A of their tax return. With the CARES Act, for gifts made in 2020 only, taxpayers have been granted an above-the-line charitable deduction of up to $300, even if they do not itemize. This only applies to cash gifts made directly to a public charity in 2020. It does not apply to gifts made to a Donor Advised Fund supporting charity.

Finally, with the exemption of Required Minimum Distributions (RMD) from IRAs and 401(k)s this year, there will likely be a subsequent drop in donations received by charitable organizations. Previously, taxpayers subject to RMD rules could make a Qualified Charitable Distribution (QCD) by distributing up to $100,000 of their RMD directly to charity, avoiding the recognition of that income. With RMDs now exempted, charitable giving for 2020 will likely be down significantly. Any charitable giving taxpayers are willing to make this year will certainly be well received.

Business as (un)usual

Sand Hill is continuing to (remotely) work on your behalf with portfolio servicing, support and planning. Please contact us with any questions, or if you’d like more information on any of these areas we have covered here. We care about our client families during this time and always. Be well, safe and healthy!

1 – Sources: IRS, Franchise Tax Board

2 – On March 21, 2020 Congress signed into Law the Coronavirus Aid, Relief and Economic Security (CARES) Act. https://www.congress.gov/bill/116th-congress/senate-bill/3548/text

Articles and Commentary

Information provided in written articles are for informational purposes only and should not be considered investment advice. There is a risk of loss from investments in securities, including the risk of loss of principal. The information contained herein reflects Sand Hill Global Advisors' (“SHGA”) views as of the date of publication. Such views are subject to change at any time without notice due to changes in market or economic conditions and may not necessarily come to pass. SHGA does not provide tax or legal advice. To the extent that any material herein concerns tax or legal matters, such information is not intended to be solely relied upon nor used for the purpose of making tax and/or legal decisions without first seeking independent advice from a tax and/or legal professional. SHGA has obtained the information provided herein from various third party sources believed to be reliable but such information is not guaranteed. Certain links in this site connect to other websites maintained by third parties over whom SHGA has no control. SHGA makes no representations as to the accuracy or any other aspect of information contained in other Web Sites. Any forward looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No reliance should be placed on any such statements or forecasts when making any investment decision. SHGA is not responsible for the consequences of any decisions or actions taken as a result of information provided in this presentation and does not warrant or guarantee the accuracy or completeness of this information. No part of this material may be (i) copied, photocopied, or duplicated in any form, by any means, or (ii) redistributed without the prior written consent of SHGA.

Video Presentations

All video presentations discuss certain investment products and/or securities and are being provided for informational purposes only, and should not be considered, and is not, investment, financial planning, tax or legal advice; nor is it a recommendation to buy or sell any securities. Investing in securities involves varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular client’s financial situation or risk tolerance. Past performance is not a guarantee of future returns. Individual performance results will vary. The opinions expressed in the video reflect Sand Hill Global Advisor’s (“SHGA”) or Brenda Vingiello’s (as applicable) views as of the date of the video. Such views are subject to change at any point without notice. Any comments, opinions, or recommendations made by any host or other guest not affiliated with SHGA in this video do not necessarily reflect the views of SHGA, and non-SHGA persons appearing in this video do not fall under the supervisory purview of SHGA. You should not treat any opinion expressed by SHGA or Ms. Vingiello as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of general opinion. Nothing presented herein is or is intended to constitute investment advice, and no investment decision should be made based solely on any information provided on this video. There is a risk of loss from an investment in securities, including the risk of loss of principal. Neither SHGA nor Ms. Vingiello guarantees any specific outcome or profit. Any forward-looking statements or forecasts contained in the video are based on assumptions and actual results may vary from any such statements or forecasts. SHGA or one of its employees may have a position in the securities discussed and may purchase or sell such securities from time to time. Some of the information in this video has been obtained from third party sources. While SHGA believes such third-party information is reliable, SHGA does not guarantee its accuracy, timeliness or completeness. SHGA encourages you to consult with a professional financial advisor prior to making any investment decision.

Recent Posts