Fueled by the advance of technology, flexibility of remote work, continued expansion of global business, and desirable cost of living tradeoffs for retirees, the ranks

Tales from the Shift: “Have Share Buybacks Peaked…?”

Published Date : November 25, 2016

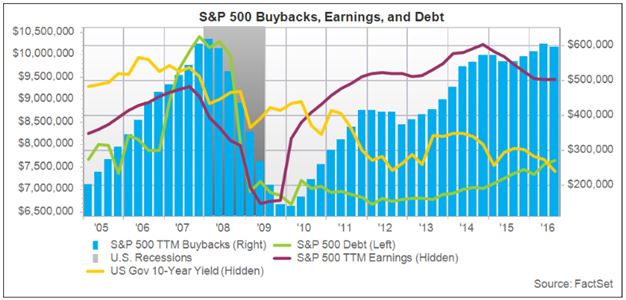

When companies have excess cash on their balance sheet, they have a few buckets they can allocate towards. However as it relates to sharing that cash with stockholders, it all comes down to buybacks and dividends. Whereas companies have long returned cash to shareholders, momentum shifted earlier this decade towards share repurchases with corporate America spending nearly $3 trillion on buybacks since 2010. In this note, we look at the share buyback component, its influence on the market and a developing change in trend.

How did buyback activity become so pervasive? In our experience, companies historically have tried to time their buybacks to take advantage of temporary weakness in their common stock. However, post the Great Recession, several prominent institutional investors insisted that capital return policies become a much larger and ongoing process. These huge asset managers began dictating to management teams that if they wanted their sponsorship, corporations needed to respond to the slower growth environment by delivering cash (a.k.a. “capital”) back to shareholders. Timing of this request was elegant given projected returns from investing in additional plant and equipment looked low in an already over-burdened landscape. It’s our view that historically low interest rates drove continual debt refinancing, providing companies the flexibility for increased borrowing with the intent to repurchase shares. The end objective, as we interpret it, was to lower the number of shares outstanding to enhance an otherwise unappealing earnings growth rate. With the stars aligned, the stage was set for what we view as one of the largest buyback cycles in history.

The share retirement process has become embraced broadly over the past decade, which continued to proliferate as borrowing costs moved close to, and at times, below zero globally. However, interest rates have started to shift higher and corporate balance sheets are no longer under-levered. Total debt for companies in the S&P 500 actually hit its highest post recession level in the second quarter of 2016, potentially causing a headwind for further issuance for share repurchases.

How important do we believe this mega-cycle of share buybacks is to the stock market? As we see it, in addition to boosting earnings growth, the enormous buyback activity produces numerous incremental perks for the stock market including:

- Reduces share price volatility acting as a shock absorber during times of weakness;

- Provides a source of liquidity for market makers, helping mitigate transactions costs;

- Reduces the dilutive effect of a growing share count when employees exercise options;

- Reduces the percentage of shares eligible for voting in the hands of external shareholders, giving management more control;

- Reduces the share count eligible to receive cash dividends (reducing the dividend burden); and

- Acts as a tool to fend off hedge funds given shorting stocks can be a fruitless exercise when a company’s share base is shrinking.

Coincidently and perhaps not surprisingly given the magnitude of this trend, most of the volatility the stock market experiences occurs during earnings season when corporations are in their quiet period and subsequently restricted from buying back their own shares.

The last buyback peak coincided with the peak in the economic cycle in 2007, causing some to draw the conclusion that the market may take a similar path. In our opinion, we are in a different environment as we don’t appear to be in a credit bubble, and economic growth should continue to drive organic earnings growth. Additionally, we think that the capital return thematic has been so ingrained into the culture at public corporations that we aren’t likely to see a big drop in buybacks overall. As an upside scenario, we believe that we could actually see renewed activity for share buybacks if our new government regime allows the nearly $1.5 trillion mountain of offshore corporate cash to be repatriated with minimal tax penalties. Such a scenario could be a win-win for our government to collect more tax dollars and for companies to maintain healthy balance sheets.

Here at Sand Hill, we sense going forward that dividend growth and sustainability could become incrementally more important factors than buybacks. It’s our opinion that the road has been paved for the transition as it’s easier to raise dividends now that the share count has been lowered! Some would say that perhaps an even more powerful indicator of positive sentiment for public companies is to keep an eye on insider share purchases by executives using their own personal money going forward.

In conclusion, companies historically tended to buy back shares when they were feeling confident about their business, but there has been a “shift” over the past decade. If buybacks slow down, we might see a little more volatility in the market on the margin. At Sand Hill, we keep a close eye on corporate and executive buyback levels factoring both as important inputs into our investment decisions. We recognize the importance of staying on top of changes in the market place so we can keep our client portfolios relevant, positioning them for anticipated movements ahead of a shift rather than behind.

Articles and Commentary

Information provided in written articles are for informational purposes only and should not be considered investment advice. There is a risk of loss from investments in securities, including the risk of loss of principal. The information contained herein reflects Sand Hill Global Advisors' (“SHGA”) views as of the date of publication. Such views are subject to change at any time without notice due to changes in market or economic conditions and may not necessarily come to pass. SHGA does not provide tax or legal advice. To the extent that any material herein concerns tax or legal matters, such information is not intended to be solely relied upon nor used for the purpose of making tax and/or legal decisions without first seeking independent advice from a tax and/or legal professional. SHGA has obtained the information provided herein from various third party sources believed to be reliable but such information is not guaranteed. Certain links in this site connect to other websites maintained by third parties over whom SHGA has no control. SHGA makes no representations as to the accuracy or any other aspect of information contained in other Web Sites. Any forward looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No reliance should be placed on any such statements or forecasts when making any investment decision. SHGA is not responsible for the consequences of any decisions or actions taken as a result of information provided in this presentation and does not warrant or guarantee the accuracy or completeness of this information. No part of this material may be (i) copied, photocopied, or duplicated in any form, by any means, or (ii) redistributed without the prior written consent of SHGA.

Video Presentations

All video presentations discuss certain investment products and/or securities and are being provided for informational purposes only, and should not be considered, and is not, investment, financial planning, tax or legal advice; nor is it a recommendation to buy or sell any securities. Investing in securities involves varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular client’s financial situation or risk tolerance. Past performance is not a guarantee of future returns. Individual performance results will vary. The opinions expressed in the video reflect Sand Hill Global Advisor’s (“SHGA”) or Brenda Vingiello’s (as applicable) views as of the date of the video. Such views are subject to change at any point without notice. Any comments, opinions, or recommendations made by any host or other guest not affiliated with SHGA in this video do not necessarily reflect the views of SHGA, and non-SHGA persons appearing in this video do not fall under the supervisory purview of SHGA. You should not treat any opinion expressed by SHGA or Ms. Vingiello as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of general opinion. Nothing presented herein is or is intended to constitute investment advice, and no investment decision should be made based solely on any information provided on this video. There is a risk of loss from an investment in securities, including the risk of loss of principal. Neither SHGA nor Ms. Vingiello guarantees any specific outcome or profit. Any forward-looking statements or forecasts contained in the video are based on assumptions and actual results may vary from any such statements or forecasts. SHGA or one of its employees may have a position in the securities discussed and may purchase or sell such securities from time to time. Some of the information in this video has been obtained from third party sources. While SHGA believes such third-party information is reliable, SHGA does not guarantee its accuracy, timeliness or completeness. SHGA encourages you to consult with a professional financial advisor prior to making any investment decision.

Recent Posts