Fueled by the advance of technology, flexibility of remote work, continued expansion of global business, and desirable cost of living tradeoffs for retirees, the ranks

Demystifying Social Security Retirement Benefits for Divorcees

Published Date : September 13, 2018

Understanding Social Security retirement benefits can be a daunting task for many, but even more so for divorcees. The eligibility rules are different when collecting a benefit on a former spouse’s employment record. The following article is meant to help demystify much of the confusion surrounding qualifying for a benefit and provide key guidelines to make the entire process as simple as possible.

First, let’s review some basics about Social Security retirement benefits. Social Security is considered an entitlement benefit, meaning as long you paid into social security for the minimum time period over the course of your working career, you are entitled to a monthly benefit upon reaching a certain age. The benefits available are structured under the premise that regardless of which spouse was the primary wage earner in a household, the non-working spouse deserves a personal benefit as well. It is also important to note that Social Security is gender-neutral. While many of the rules date back to a time when most households had one primary wage-earner, all of the following rules apply equally to divorced men and divorced women.

How Does It Work?

If your ex-spouse is still living, you are eligible to receive a benefit as long as you satisfy the following parameters:

- The marriage lasted 10 years or longer

- Your divorce has been finalized for at least 2 years

- You are currently unmarried (it does not matter if your ex-spouse remarried)

- You are age 62 or older

- Your ex-spouse is entitled to Social Security retirement benefits

If all the above requirements are satisfied, you will be eligible for 50% of your ex-spouse’s benefit at his/her full retirement age (FRA) as soon as you reach your FRA. You have the option to begin receiving benefits when you turn age 62, however the benefit amount will be permanently reduced from what you would have collected if you waited until your FRA (in other words, less than the 50% of your ex-spouse’s benefit at his/her FRA) — more on this concept shortly. It does not matter if your ex-spouse has not actually reached FRA, or if he/she is still working. This can be a confusing concept so here is an example:

John is 65 and Jane is 66. They were married for 15 years, divorced for the last 5 years, and John is now re-married. His FRA is 66 and at that age, he’ll be eligible for $2,000 per month in benefit. Even though John has not yet reached his FRA, since Jane is already 66 (her FRA), she can start collecting $1,000 per month. It also does not matter that John is remarried.

When Should You Start Collecting?

The minimum age to begin collecting on your ex-spouse’s record is when you turn age 62. If you defer your benefit for one or more years up to your personal full retirement age, you will earn a higher benefit! If you initiate the benefit at the earliest age of 62, you permanently reduce your monthly benefit by approximately 30%, depending on when you were born. While there is no official maximum age to start collecting, it does not make financial sense to commence collecting any time after your FRA, as the benefit only increases from age 62 to your FRA, but not beyond. This is very different from standard Social Security retirement benefits, where the benefit amount increases every year until age 70.

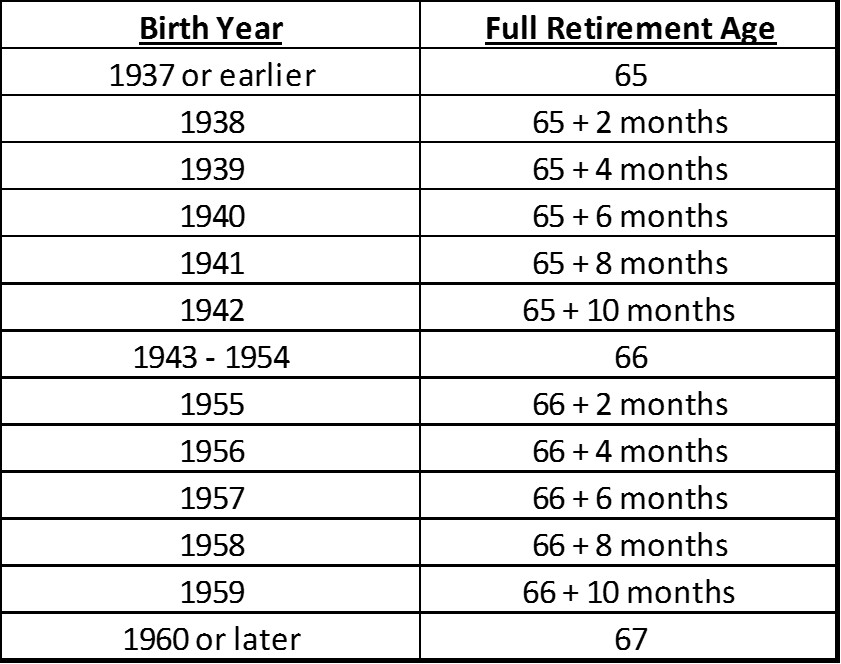

Each person’s full retirement age is set by the Social Security Administration based on your year of birth, and it is broken down on the following chart:

Source: SSA

Whose Benefit Will You Collect?

The Social Security Administration will only pay you the benefit attributable to one individual’s earnings record at a time. If the benefit amount resulting from your personal earnings record is higher than the 50% of your ex-spouse’s benefit, you will only receive your benefit, not theirs. In short, you only collect which ever benefit is higher.

Let’s consider an example: Your first marriage lasted 11 years, your second marriage lasted 12 years and you separately satisfy all the qualification rules in relation to both prior marriages. Your personal earnings record provides you with $1,500 per month in benefit. From your ex-spouses, you are eligible for $1,000 per month (50%) of former spouse #1’s benefit, and $1,700 per month (50%) of former spouse #2’s benefit. In this scenario, you would collect the largest benefit, or $1,700 per month associated with former spouse #2.

Impact If Your Ex-Spouse Dies

You can qualify for survivor (or widow) benefits on an ex-spouse’s record, even if he/she dies after the divorce is final. The specifics to qualify for survivor benefits are listed below:

- Your marriage lasted at least 10 years

- You are currently 60 years or older (50 if disabled)

- Your own retirement benefit is less than the 50% you are eligible for on your ex-spouse’s record

Lastly, if you were to remarry and the new marriage takes place after you turn 60 (or 50 if disabled), you can still collect the survivor benefit on your ex-spouse’s record. If you remarry before age 60 (or 50 if disabled), then unfortunately, you forfeit the benefit.

If a re-marriage takes place which nullifies a survivor benefit, at that point any future benefit would revert to your own personal record, or that of your new spouse once you reach your 10-year anniversary.

This could explain the more recent trend of senior citizens who live together unmarried. While everyone’s circumstances are unique, one possible explanation for this trend is related to how Social Security benefits are handled if the recipient were to remarry. If a re-marriage takes place which nullifies a survivor benefit, at that point any future benefit would revert to your own personal record, or that of your new spouse once you reach your 10-year anniversary. In the case where the ex-spouse is still living, then remarriage at any age would nullify the spousal benefit.

Other Considerations

“File & Suspend” still exists for a select few!

If you were born before January 2, 1954, you are still eligible for the “file and suspend” strategy that was eliminated for everyone else by the Bipartisan Budget Act of 2015. When implementing this tactic, those who qualify have the option to take the divorced spousal benefit and delay receiving your personal retirement benefit. And if you delay to your 70th birthday (allowing your personal benefit to increase up to this point), then assuming it is higher than what you are currently collecting on your ex-spouse’s record, you can switch over to your personal benefit going forward. It is a great strategy that really maximizes your aggregate Social Security benefit.

How do government pensions impact your Social Security benefit?

If you’ve previously worked at a job that was not covered by Social Security (meaning you did not pay Social Security taxes through your paycheck), the Social Security benefit you are eligible for is typically reduced by 2/3rds on every dollar of government pension income you concurrently collect. This could have major ramifications on retirement cash flow projections, so it is critical to ensure the correct income sources are reviewed during the planning process.

What if you or your ex-spouse changed your legal name?

If a name change has taken place, be sure to update the Social Security Administration so any future earnings are attributed to your record. It is also prudent to retain your ex-spouse’s Social Security number, pre and post-divorce legal name, date of birth, place of birth, names of his/her parents and final divorce documents for the purposes of proving your eligibility, especially if you are many years away from qualifying for benefits.

What if your former spouse gets remarried?

Referencing the earlier example of Jane and John, John’s re-marriage had zero impact on Jane’s eligibility. In fact, an individual could conceivably have multiple ex-spouses collecting on his/her record. This concept was exemplified by the late comedian Johnny Carson, who was married a total of 4 times, of which 3 marriages lasted more than 10 years (the 4th marriage lasted just shy of the 10-year mark). Those 3 former spouses were eligible to collect a spousal benefit on his record, meaning as much as 250% of Mr. Carson’s benefit was being paid concurrently (100% to him plus 3 ex-wives each collecting 50% of his benefit). The key takeaway with this example is any benefits that you as the divorced spouse might be entitled to will not be affected by the benefits paid to your ex-spouse, or any of his/her other ex-spouses.

Final Thoughts

Social Security retirement benefits are confusing on their own and inserting the added complexities of the post-divorce landscape only complicates the process further. Be sure to consult with your Sand Hill Wealth Manager to help you navigate the many speed bumps and road blocks associated with applying for benefits. By demystifying the process, we can help analyze and strategize for the most optimal path for you and your family.

Source: Social Security Administration (SSA)

Articles and Commentary

Information provided in written articles are for informational purposes only and should not be considered investment advice. There is a risk of loss from investments in securities, including the risk of loss of principal. The information contained herein reflects Sand Hill Global Advisors' (“SHGA”) views as of the date of publication. Such views are subject to change at any time without notice due to changes in market or economic conditions and may not necessarily come to pass. SHGA does not provide tax or legal advice. To the extent that any material herein concerns tax or legal matters, such information is not intended to be solely relied upon nor used for the purpose of making tax and/or legal decisions without first seeking independent advice from a tax and/or legal professional. SHGA has obtained the information provided herein from various third party sources believed to be reliable but such information is not guaranteed. Certain links in this site connect to other websites maintained by third parties over whom SHGA has no control. SHGA makes no representations as to the accuracy or any other aspect of information contained in other Web Sites. Any forward looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No reliance should be placed on any such statements or forecasts when making any investment decision. SHGA is not responsible for the consequences of any decisions or actions taken as a result of information provided in this presentation and does not warrant or guarantee the accuracy or completeness of this information. No part of this material may be (i) copied, photocopied, or duplicated in any form, by any means, or (ii) redistributed without the prior written consent of SHGA.

Video Presentations

All video presentations discuss certain investment products and/or securities and are being provided for informational purposes only, and should not be considered, and is not, investment, financial planning, tax or legal advice; nor is it a recommendation to buy or sell any securities. Investing in securities involves varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular client’s financial situation or risk tolerance. Past performance is not a guarantee of future returns. Individual performance results will vary. The opinions expressed in the video reflect Sand Hill Global Advisor’s (“SHGA”) or Brenda Vingiello’s (as applicable) views as of the date of the video. Such views are subject to change at any point without notice. Any comments, opinions, or recommendations made by any host or other guest not affiliated with SHGA in this video do not necessarily reflect the views of SHGA, and non-SHGA persons appearing in this video do not fall under the supervisory purview of SHGA. You should not treat any opinion expressed by SHGA or Ms. Vingiello as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of general opinion. Nothing presented herein is or is intended to constitute investment advice, and no investment decision should be made based solely on any information provided on this video. There is a risk of loss from an investment in securities, including the risk of loss of principal. Neither SHGA nor Ms. Vingiello guarantees any specific outcome or profit. Any forward-looking statements or forecasts contained in the video are based on assumptions and actual results may vary from any such statements or forecasts. SHGA or one of its employees may have a position in the securities discussed and may purchase or sell such securities from time to time. Some of the information in this video has been obtained from third party sources. While SHGA believes such third-party information is reliable, SHGA does not guarantee its accuracy, timeliness or completeness. SHGA encourages you to consult with a professional financial advisor prior to making any investment decision.

Recent Posts